In this section, we explore the dynamics of entry and exit events in firms and their impact on sectoral sales time series. This is crucial for extending the formal framework to account for the active or inactive status of firms over time.

Consider the decomposition of sectoral sales time series Spt:

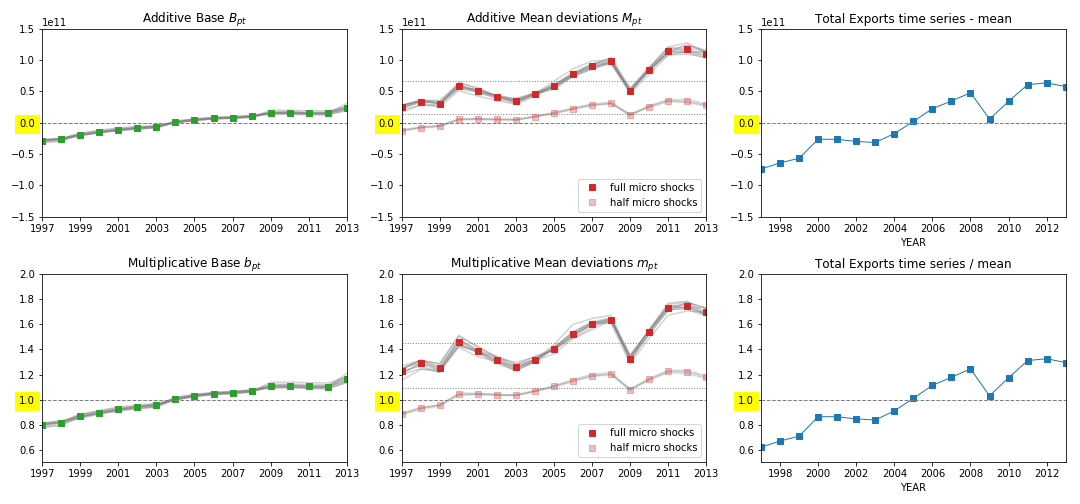

Spt=Sˉp+ΔSpt=Sp0+Bpt+Mpt+Ept

Sˉp: The observed mean of the time series.

ΔSpt: Deviations from the mean level.

Bpt: Accounts for nominal fluctuations, especially due to entry and exit events.

Mpt: Captures contributions related to comovements.

Ept: Captures contributions related to sectoral idiosyncrasies.

The relationship implies Spt−Sp0=Bpt+Mpt+Ept, where Sp0 is observed when all fluctuations are removed. Note that Sˉp includes the net mean of the B,M,E terms.

ϵpt: A random variable with mean zero and std = 1.

This implies:

log(Spt/Sp0)=bpt+mpt+σpϵpt

The relationship to nominal accounts is:

Spt=Sp0+Bpt+Mpt+Ept=Sp010bpt+mpt+σpϵpt

Consider a thought experiment where fluctuations are 'turned on' from zero to actual magnitudes. Initially, log(Spt/Sp0)=bpt. As shocks are activated, we observe differences as:

log(Spt′)−log(Spt)=δpt=mpt+σpϵpt

The width of this time series is σ=σδ2+σb2. Depending on the magnitude of micro shocks and firm dynamics, different sources may explain observed aggregate volatility.

For mild sectoral fluctuations, the covariance matrix elements are:

Each element involves nine terms, combinations of b,m,σϵ. For P parts, the total variance sums 9P2 contributions, with different combinations and cross terms contributing to the aggregate variance.